Since listing in 1994, Australian biotech company CSL has powered ahead to become our second largest company by market cap. Lying just ahead is the Commonwealth Bank. But with a more compelling growth story, it’s probably just a matter of when, not if, CSL will hit the front.

We have profited handsomely from the ownership, on behalf of our investors, of CSL (ASX:CSL) in The Montgomery Fund and The Montgomery [Private] Fund, so we are cheering it along as it grows daily in market value.

Australian biotech company CSL Limited was founded in 1916 and researches, develops, manufactures, and markets products to prevent and treat life-threatening illnesses, immunodeficiencies, and bleeding disorders; it also makes influenza vaccines.

The Commonwealth Bank (ASX:CBA), on the other hand, needs very little introduction, being Australia’s largest bank and, since the GFC at least, its most profitable – thanks in no small part to its very opportunistic (read cheap) acquisition of Bankwest during the depths of the GFC.

As an aside, CBA purchased Bankwest for $2.1 billion in October/November 2008 without the usual regulatory and political debate that would surround one bank taking over another. At the time, it struck me as a rescue of a failing bank with the CBA probably being directed by the government to prevent a destablisation of Australia’s financial system. The CEO at the time noted: “Bankwest provides us with a significant opportunity to further enhance the group’s business in the fast-growing Western Australia market”.

There was nothing ‘fast growing’ about Western Australia during the GFC.

But this is not a blog about the CBA. It’s about the relative valuations we now observe between CSL and the CBA.

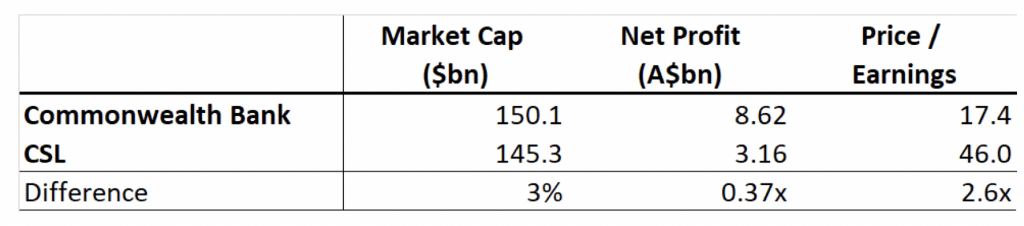

The Commonwealth Bank is one of Australia’s largest listed companies and trades at a market capitalization of A$150 billion and on the highest PE multiple of just about any bank in the world at 17.4x. The bank is also expected to generate a net profit in 2020 of A$8.6 billion.

Meanwhile, CSL’s market capitalization is $145 billion, just 3 per cent lower than the Commonwealth Bank. And yet CSL’s net profit for 2020 is forecast to be just A$3.2 billion, or just over one third (0.37x) of Commonwealth Bank. Of course, the difference can be explained by low rates and growth expectations but with the price to earnings ratio of CSL being 2.6 times the earnings ratio of CBA, one has to ask whether CSL’s growth is going to be at least double that of CBA over the medium to long term.

In the last four years CSL has grown its net profit after tax by an average of 8.6 per cent per annum, nominally 3.3 times greater than the CBA, which is going backwards. CBA has seen its earnings per share decline from $5.57 per share in 2015 to $4.80 last year, growth of negative 3.7 per cent per annum. On that basis, it seems CSL’s assault on the CBA’s market capitalization might be justified but keep in mind the cyclicality of outperformance and underperformance.

The Montgomery Fund and Montgomery [Private] Fund own shares in CSL. This article was prepared 07 February with the information we have today, and our view may change. It does not constitute formal advice or professional investment advice. If you wish to trade CSL you should seek financial advice.